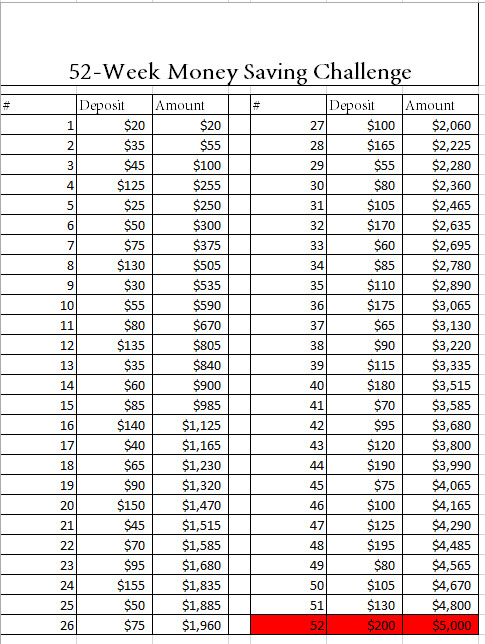

Whether it’s a house, a new vehicle, or other lending options, having a down payment is always a great first step. In this 52-week challenge you will begin saving a little at a time to accumulate $5000 this year! Here’s how it works, every week you deposit a different amount into your savings account. As the weeks go on you begin to build a steady base little by little. At the end of the year you will have saved $5000 if done correctly. You can also add to the numbers shown below if you’d like to save more than $5000. Simply take the additional amount you would like to save, and divide it by 52. Now add that number to each of the deposit amounts for the year and you have your game plan.

$5000 is a substantial sum of money that offers endless potential, so here are some ideas to get you started!

Vacation: Take a break and enjoy an exciting new destination with your family! Cruises start at less than $700/person, and a week in Florida typically runs $4000+ for a family of four.

New Vehicle: You can either purchase a used vehicle with the $5000 (or less), or you can use the $5000 to put a down payments on a more expensive vehicle you’ve had your eye on.

Down Payment on a Home: With $5000 on top of your current savings, this may finally be the year you decide to become a homeowner! There are many lending options to help you purchase your new home that can work together with your budget.

Wedding: A little creativity may be involved but the celebration can go on! With the largest event expenses being the venue, food, and photographer, finding inventive shortcuts can turn $5000 into the wedding of your dreams!

No matter what you’re saving toward Iowa State Bank & Trust Company is here to help you achieve it! Stop by the bank or call us today at (641) 472-3161 to get started with one of our convenient savings accounts.

You must be logged in to post a comment.